Here is what I found interesting in today’s world of retail:

Over half of Americans prefer all at once TV show releases vs staggered. Link

Alibaba used AI for New York Fashion Week looks. Link

Millennials are taking over fashion too. Link

Alibaba acquires largest rival. Link

Amazon and Roku battle for your TV. Link

Streaming music makes up 80% of the music industry revenue. Link

The world’s most expensive retail playground is struggling. Link

Everyone loves the lending game, Stripe Capital is the latest to enter the game. Link

Influencers are seeing less engagement with the disappearance of likes. Link

Facebook dating now challenging the IAC dating monopoly. Link

43% of survey respondents interested in Disney + streaming. Link

Amazon now testing the “New” badge. Link

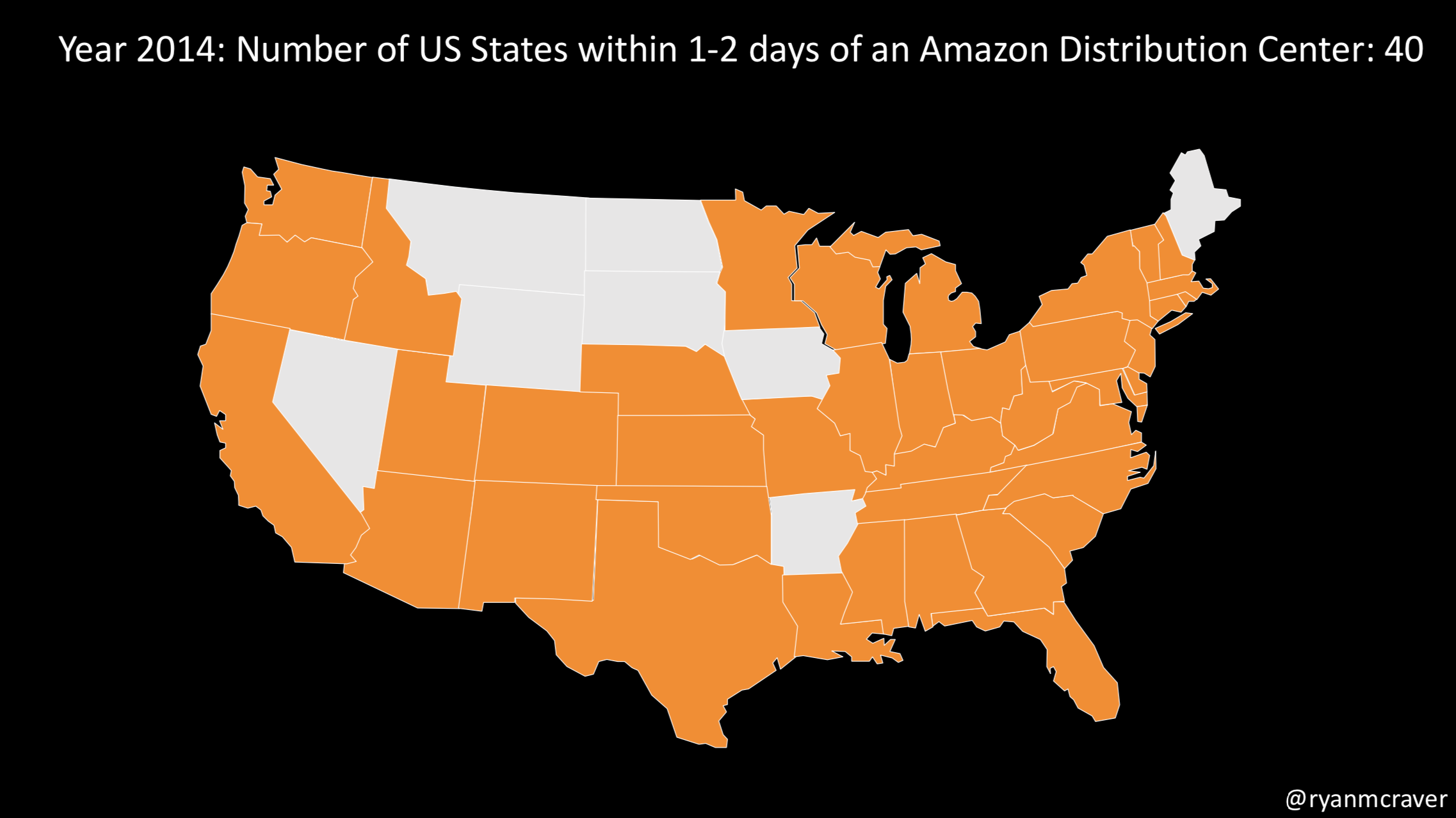

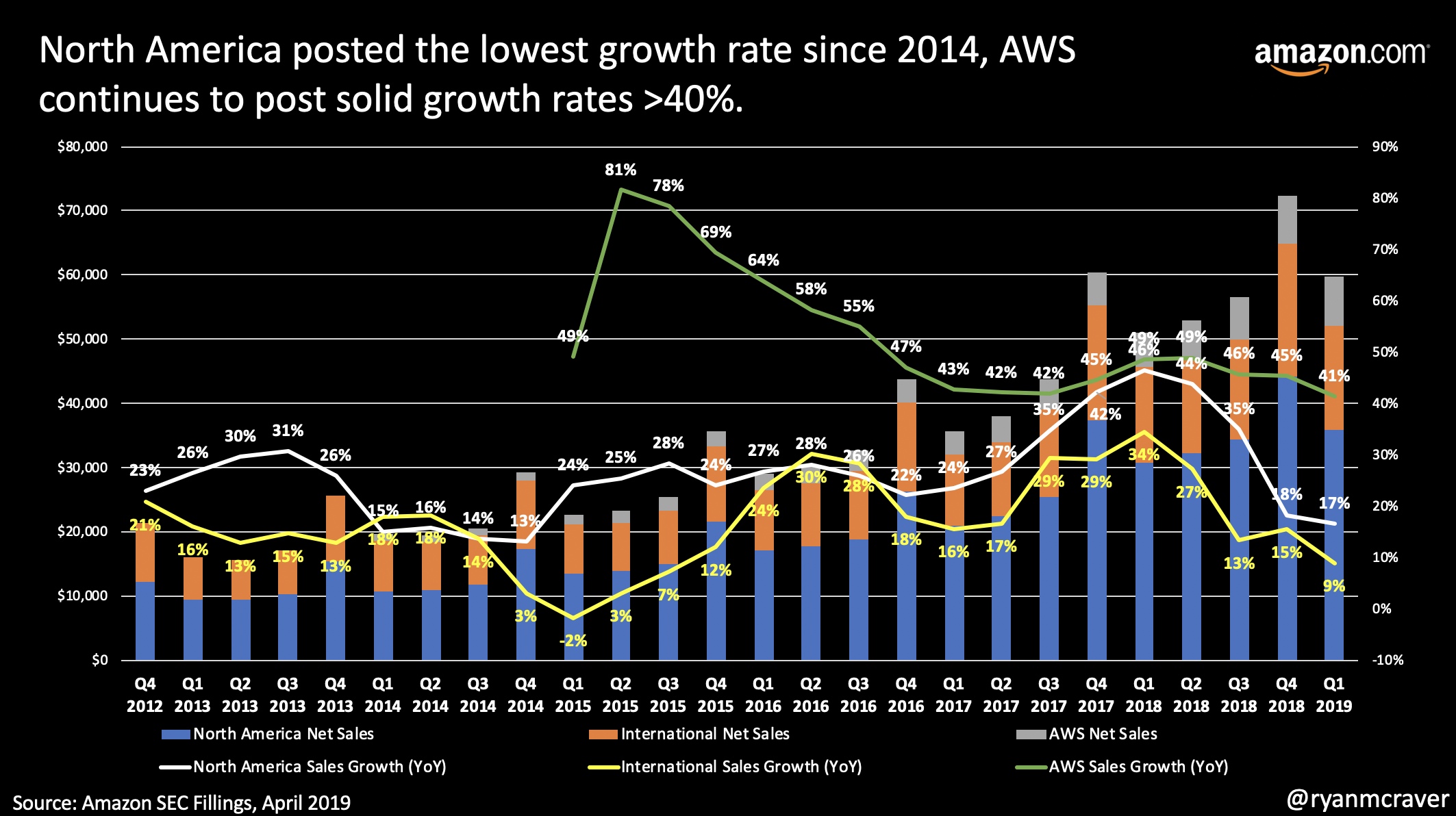

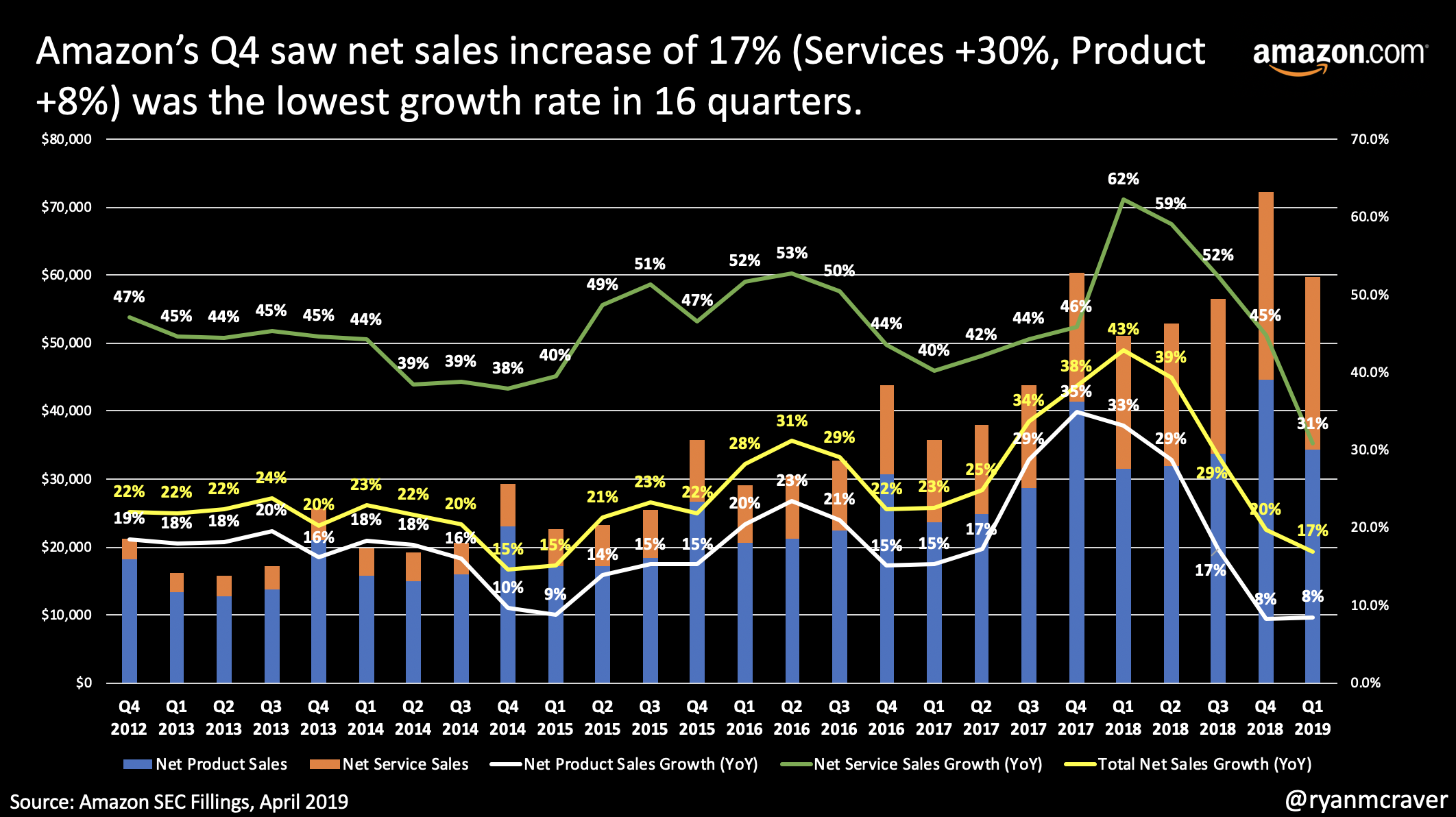

Amazon pushes faster shipping at all costs. Link