Disclaimer: Long position was sold today before earnings but will be re-establishing position shortly.

Robinhood announced another quarter of earnings this evening. Prior overviews are here, here, and here.

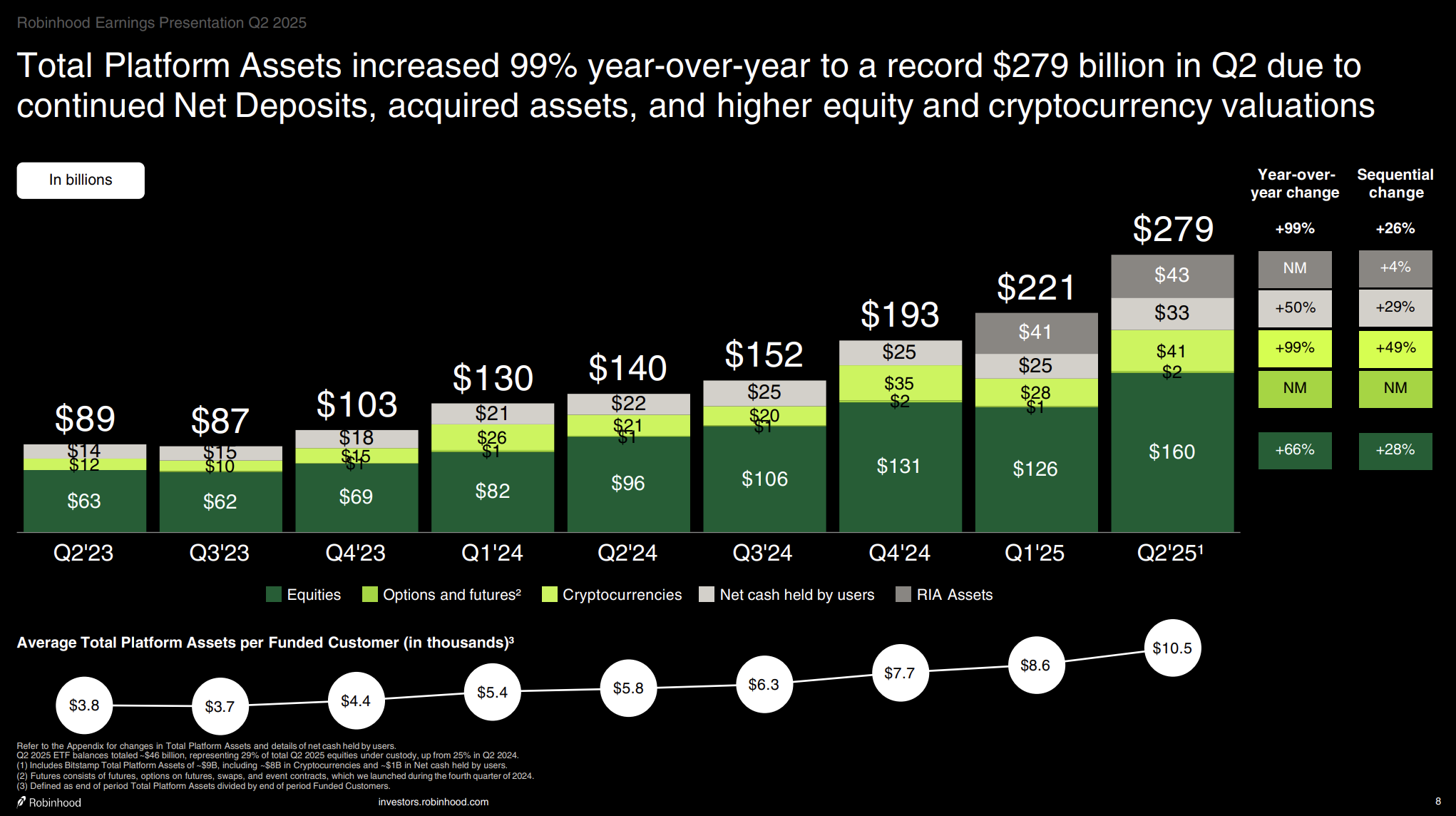

Assets Under Custody/Net Deposits - Assets saw an increase of 99%, an acceleration from 70% in the latest quarter versus last year. Keep in mind that a significant portion of the increase was due to TradePMR acquisition and the higher valuations of equity of cryptocurrency.

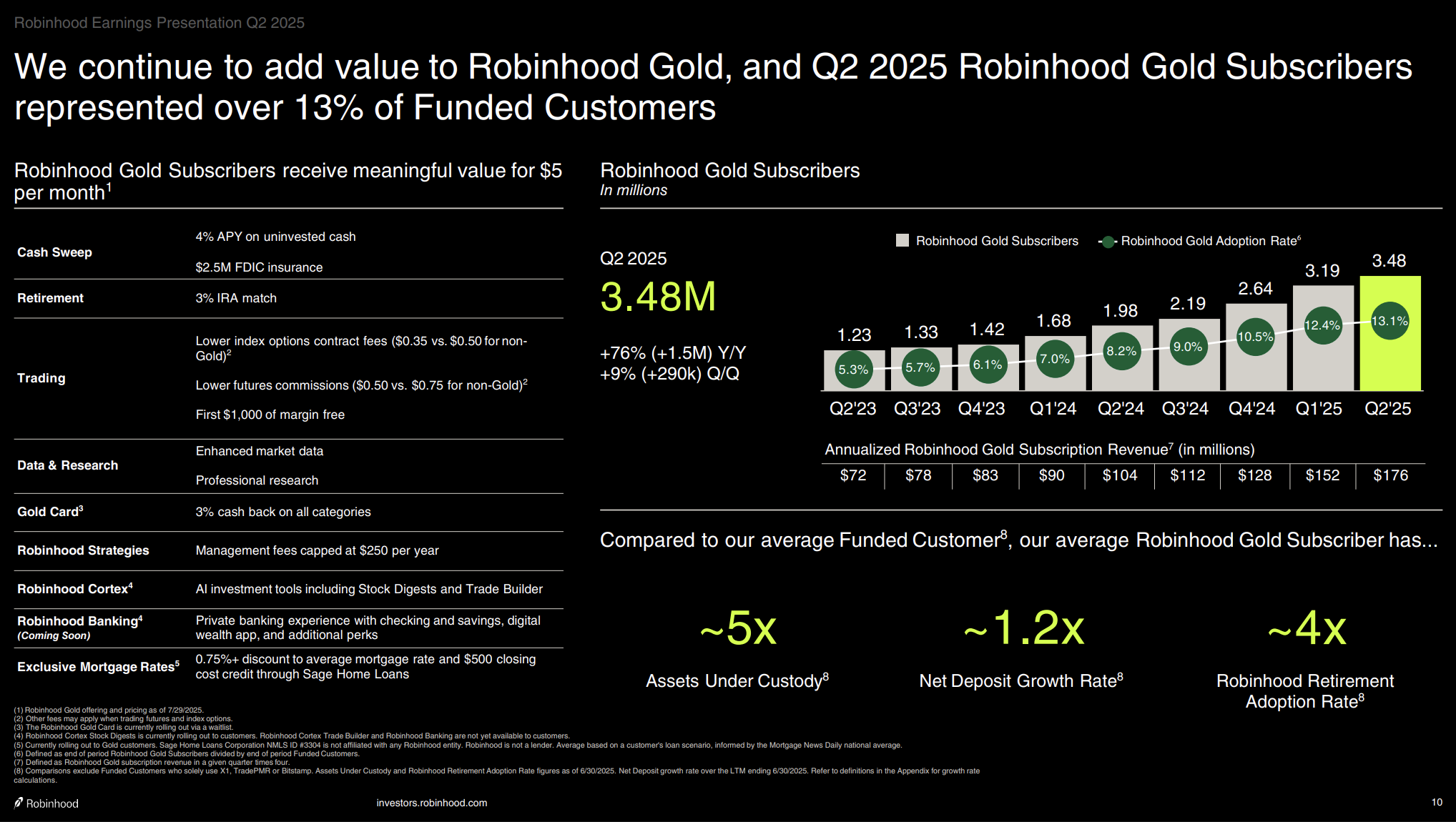

Gold Stickiness - The stickiness continues. Last 3 quarters adoption rate has grown from 10.5% to 12.4% to 13.1%. The subscriber base continues to grow and that stickiness leads to higher activity and lower churn. Note that the credit card is now up from 200k subs to over 300k subs this quarter. The CFO noted they will continue to grow credit card subs yet will do so with a “measured” approach.

Net Deposits - A deceleration here as they pulled back slightly in the promotional activities from 37% to 25% year over year.

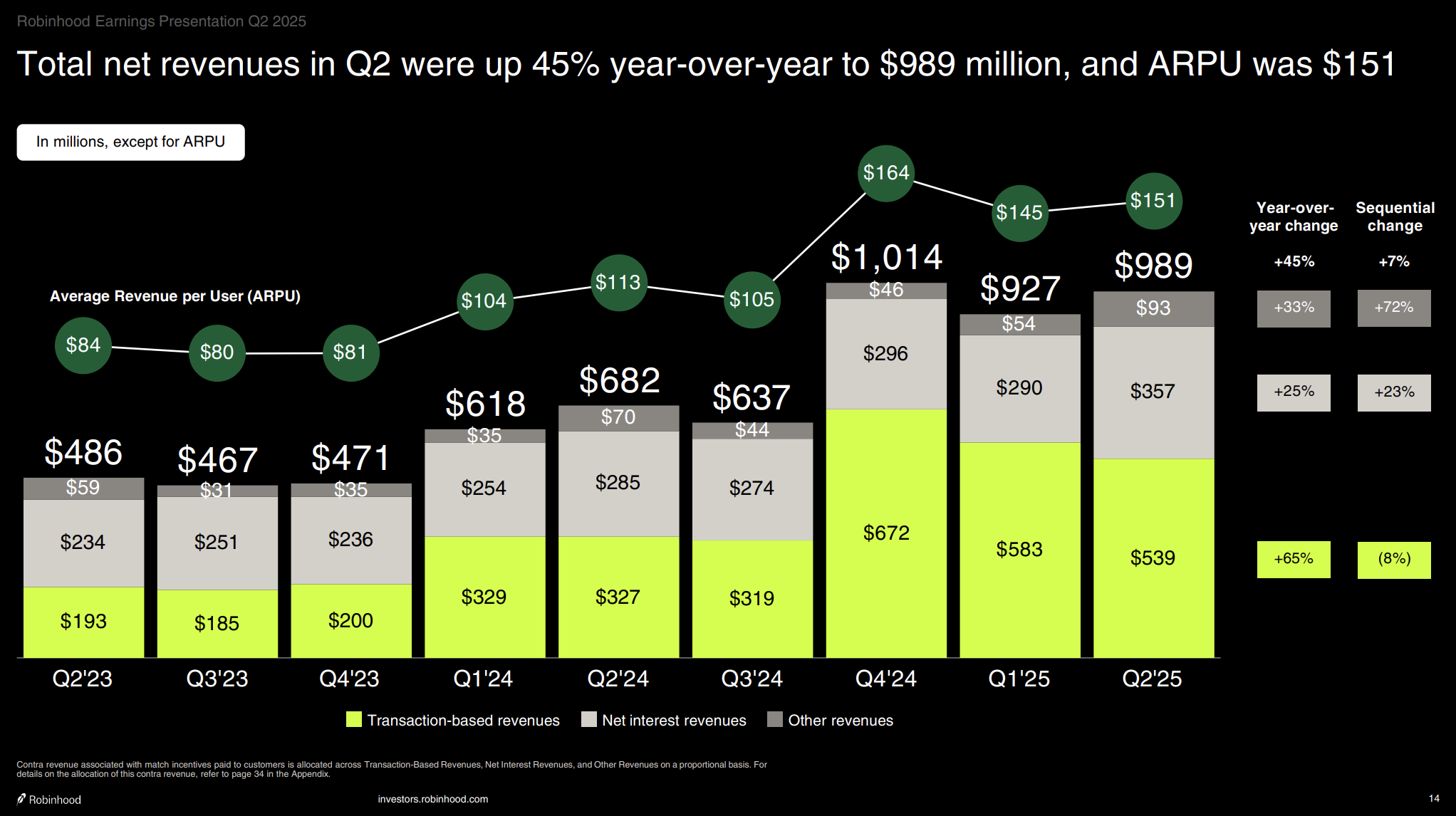

Average Revenue Per User (ARPU) Growth - Whilst the average is down slightly from Q1, the yearly growth figures remain incredibly healthy.

Bottom Line: Net deposits continue to grow albeit a bit slower, Gold subscribers continue to drive stickiness all as the revenue diversifies well outside of just crypto via credit cards, options, staking and eventual launch of banking. Robinhood continues to drive industry change and build complementary businesses within the core US market as well EU market. No reason not to remain long in my opinion despite the aggressive share price increases over the last several months.