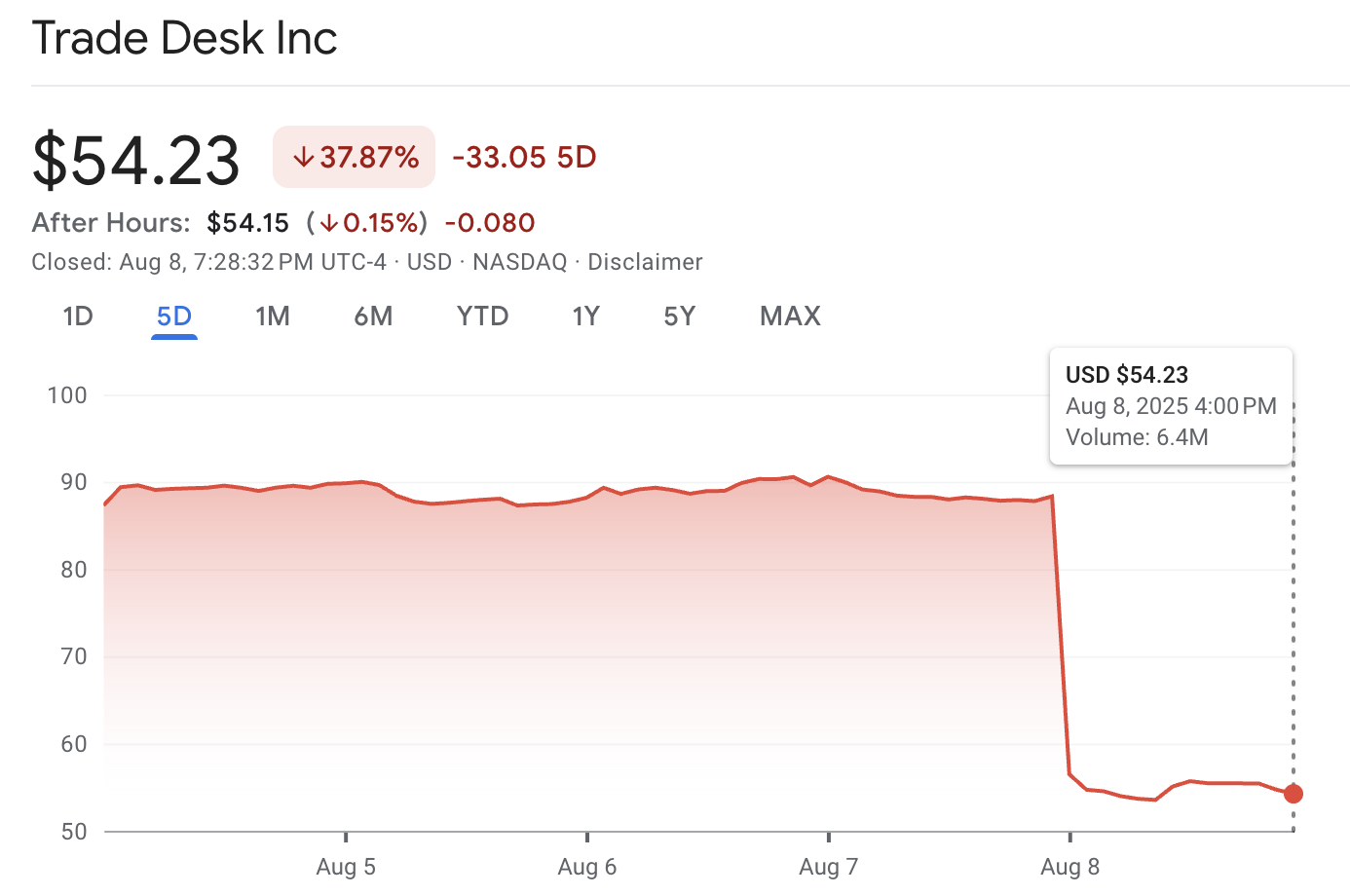

Trade Desk’s stock plummeted nearly 38% following its most recent earnings release. Much of the conversation on Wall Street centers on the view that Amazon is increasingly taking market share from Trade Desk, thanks to the fast growth of Amazon's DSP platform, the rise of Prime TV, and Amazon's unique ability to easily attract small and medium-sized brands. Unlike Trade Desk, which traditionally targets larger agency groups and major brands, Amazon's advertising solution appeals to a broader client base, making it remarkably easy for smaller advertisers to launch campaigns with just a few clicks.

However, it's important to look beyond Amazon’s competitive strength. The more significant underlying challenge for Trade Desk may be the sheer volume of digital ad inventory now flooding the market. Recent developments, such as Netflix entering the ad-supported streaming space and the accelerating shift toward connected and streaming TV, have resulted in nearly a 40% increase in available ad inventory. As a result, this glut in supply has driven down the cost per mille (CPM)—the price paid to reach 1,000 viewers. Where major streaming platforms once saw CPMs above $50 in 2023, today the average falls below $30.

While competitive pressures from Amazon are real, investors considering Trade Desk should recognize that the broader market dynamics—namely, the rapid expansion of streaming ad inventory and the resulting decline in CPMs—pose a more fundamental challenge to revenue growth and profitability. I wouldn’t be a buyer at these levels.

Disclosure: No position in Trade Desk.