February 2026 was a watershed month for large language models: growth is still explosive, but power is clearly consolidating around a handful of consumer chatbots and enterprise platforms.

Market size and momentum

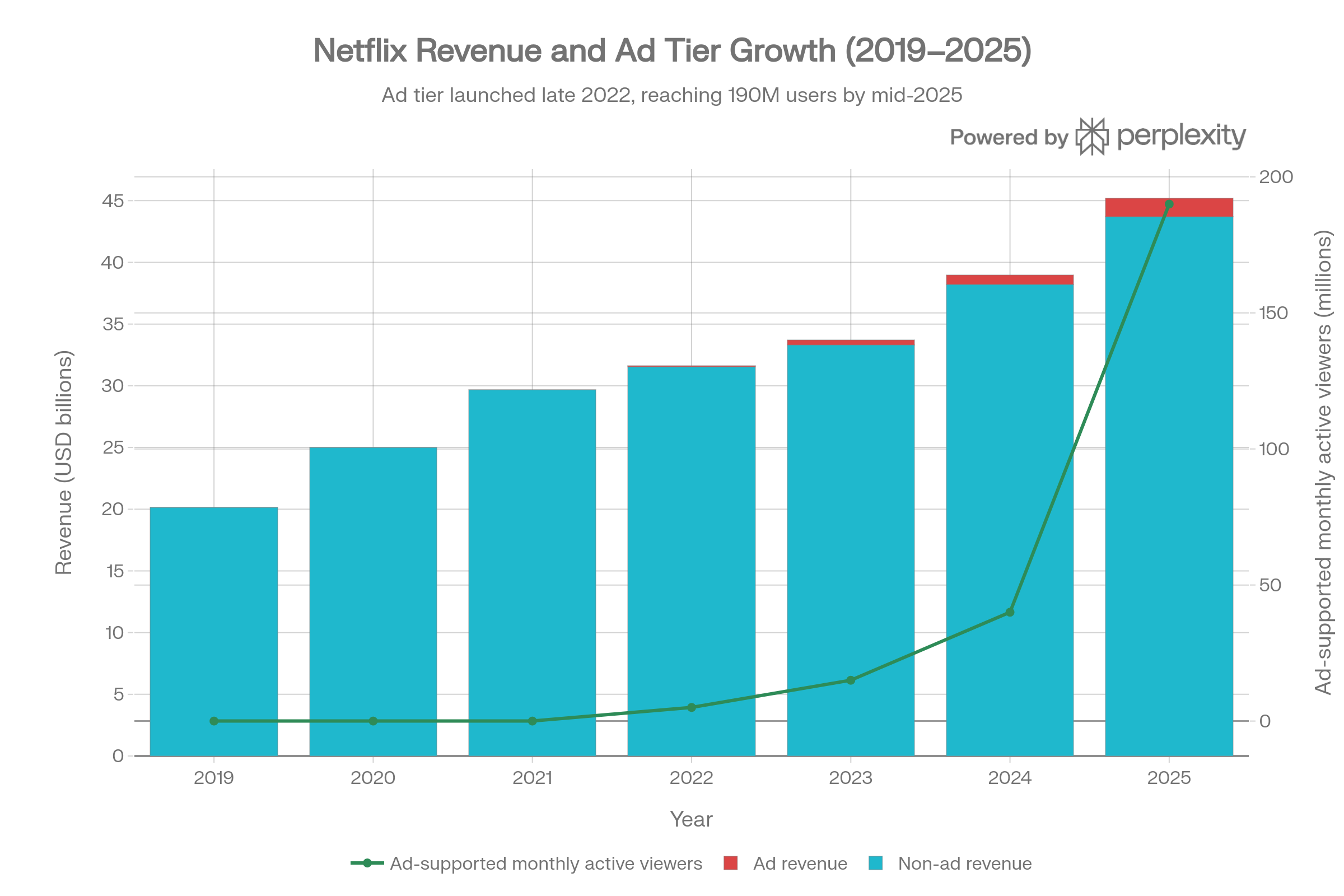

The wider LLM and generative AI market continues to expand at a double‑digit clip, driven by enterprise adoption and AI‑native products. Analysts now peg the global LLM market in the mid–single digit billions, with forecasts pushing it toward tens of billions by the early 2030s. Transformers remain the dominant underlying technology, controlling a large share of generative AI revenue across language, vision, and multimodal workloads.

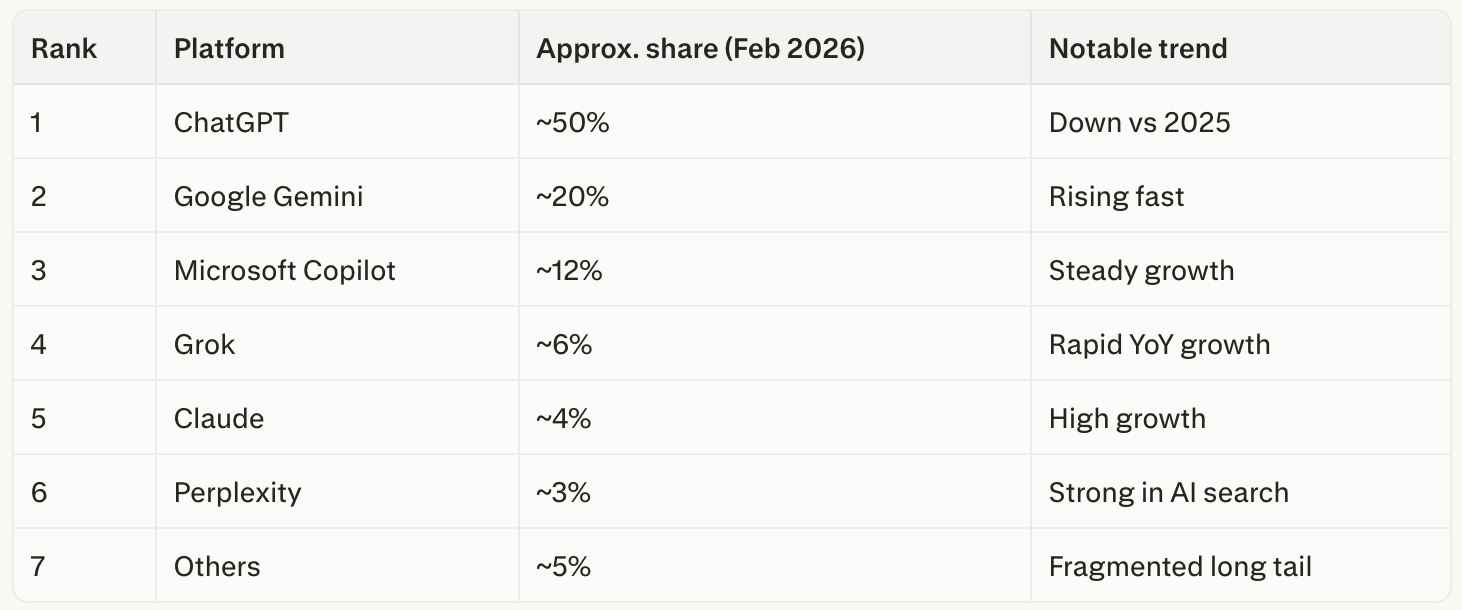

February 2026: Consumer LLM usage

On the consumer side, February 2026 confirmed that we’re in an oligopoly, not a monopoly. ChatGPT remains the primary entry point for most users, but its share is steadily eroding as Gemini, Copilot, and a long tail of vertical assistants mature.These ranges blend app‑store share, web traffic, and AI search data; they are best interpreted as directional rather than precise.

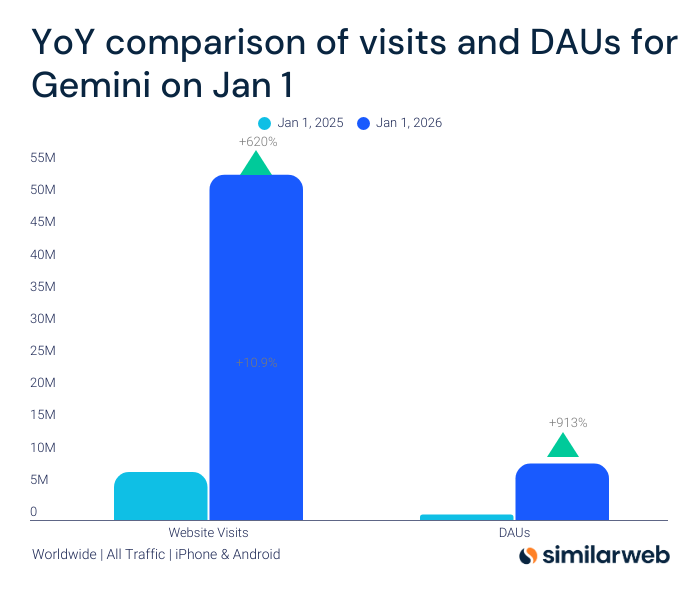

Gemini’s February Breakout

If February had a single headline, it was Gemini’s acceleration. In AI search share, Gemini has broken into the high teens to around 20%, up significantly year‑over‑year. Mobile usage shows a similar pattern as Gemini benefits from default placement and deep integration across Android and Google Workspace. For product and growth teams, this is a clear demonstration that distribution and ecosystem lock‑in can chip away at an early‑mover advantage.

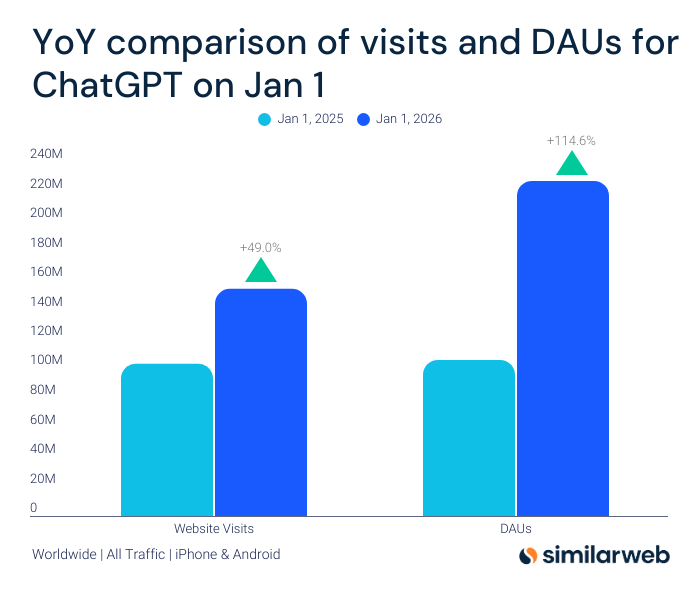

ChatGPT: From Monopoly to Anchor Tenant

OpenAI’s ChatGPT is still the anchor tenant of the LLM ecosystem, but the days of near‑70% dominance are over. Its share has fallen into the ~50% range even as absolute usage continues to grow. In AI search experiences, ChatGPT‑based offerings still command a majority, but that number has started to plateau. The implication: we’re shifting from “everyone launches on ChatGPT” to a multi‑model reality where Gemini, Claude, Copilot, and open‑source backends coexist behind the same UI.

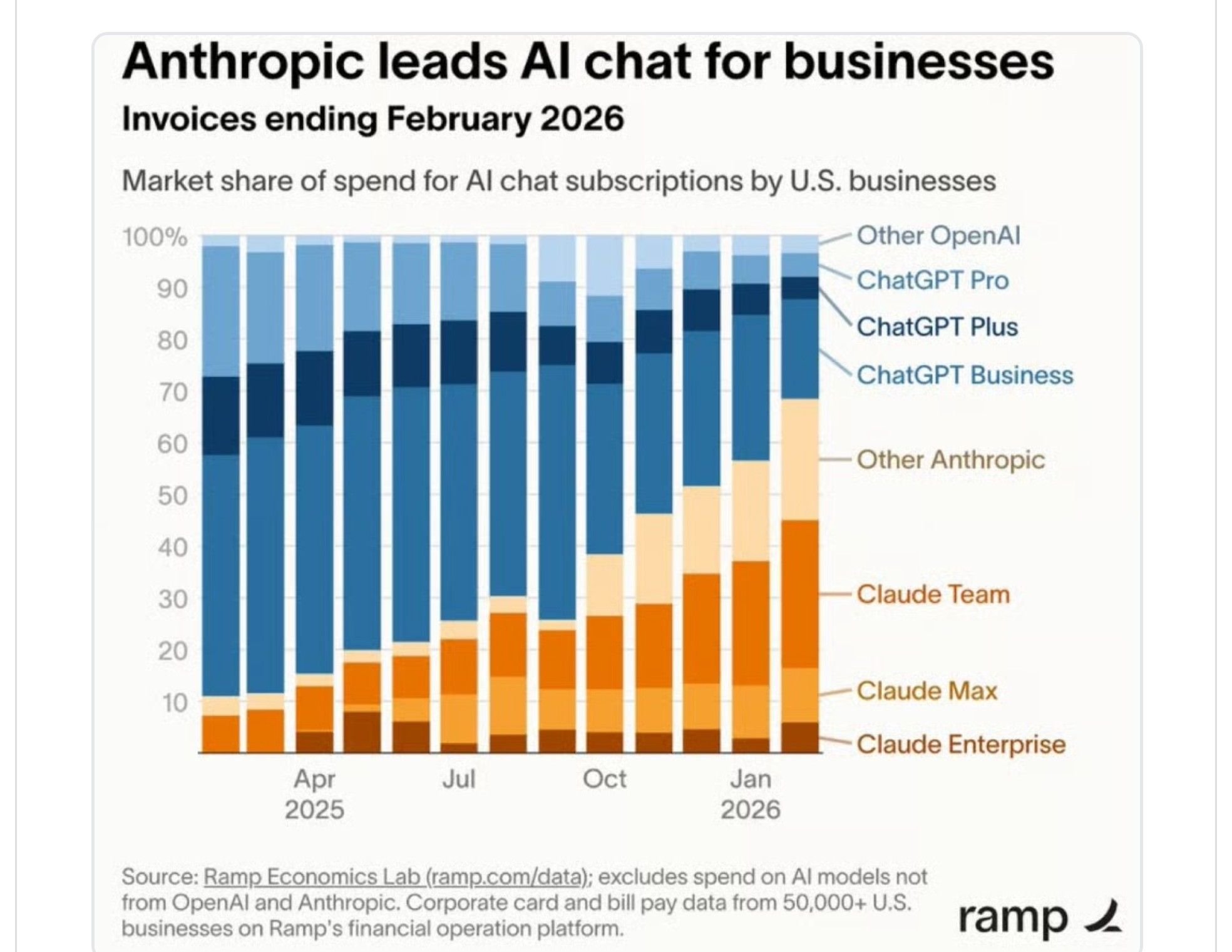

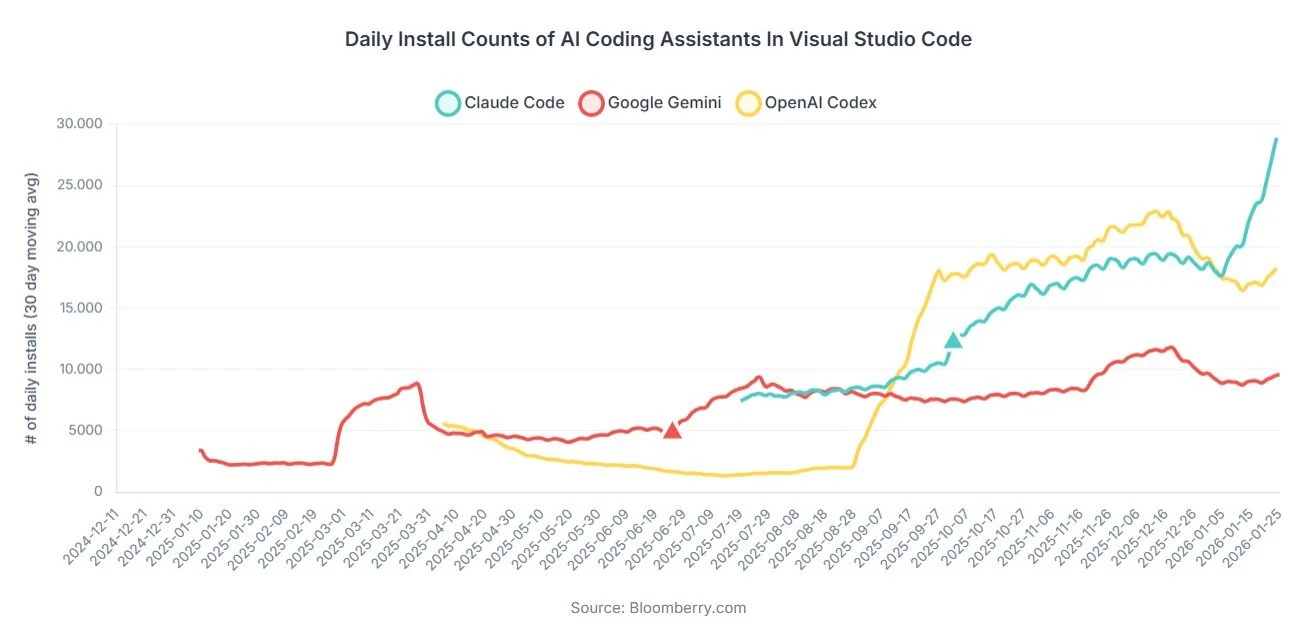

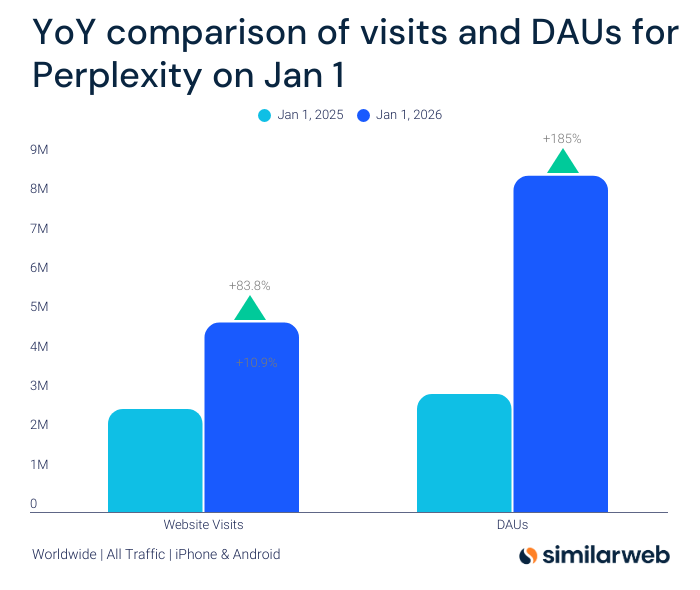

Second Wave: Claude, Copilot, Perplexity and Others

Below the top two, a second wave of fast‑growing specialists and ecosystem plays is emerging.

Microsoft Copilot sits in the low‑teens, powered by distribution inside Windows, Office, and Edge rather than pure consumer brand pull.

Claude, while still in the single digits, is one of the fastest‑growing enterprise assistants, especially for long‑context knowledge work and development.

Perplexity, with a few points of the AI search market, over‑indexes among power users looking for conversational search and source transparency.