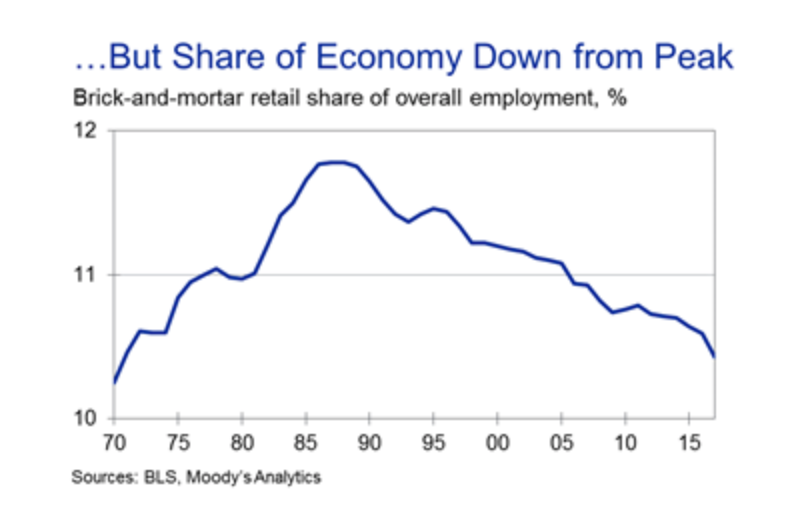

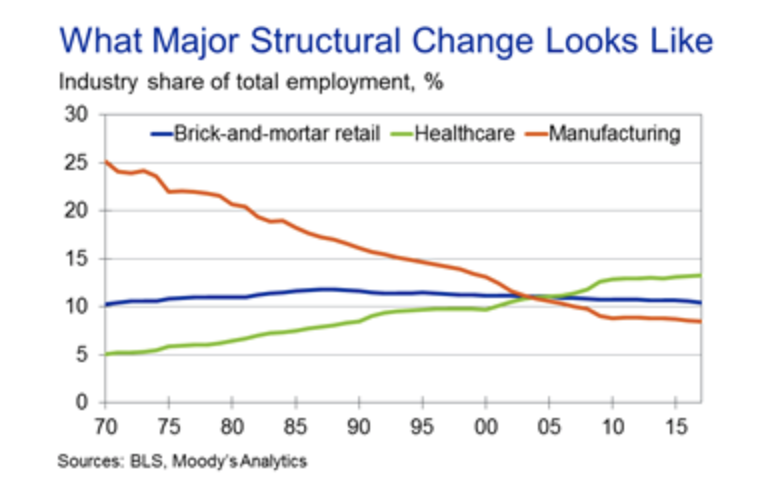

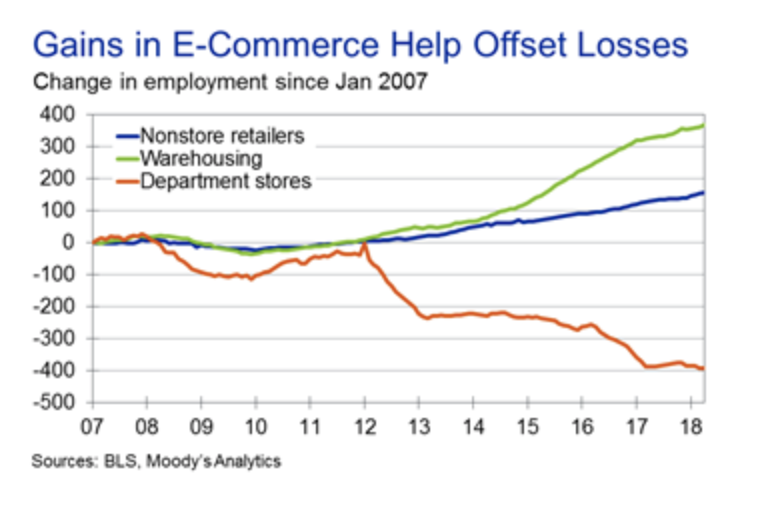

Although Moody's contends Retail isn't having a decline comparable to that of Manufacturing, the numbers show Retail becoming less impactful on the overall economy and all strength is due to ecommerce.

Your Custom Text Here

“Mortgage rates spiked in a big way today, bringing some lenders to the highest levels in nearly 7 years (you’d need to go back to July 2011 to see worse). That heavy-hitting headline is largely due to the fact that rates were already fairly close to 7-year highs, although today did cover quite a bit more distance than other recent “bad days.” ”

Mortgage rates spiked in a big way today, bringing some lenders to the highest levels in nearly 7 years (you'd need to go back to July 2011 to see worse). That heavy-hitting headline is largely due to the fact that rates were already fairly close to 7-year highs, although today did cover quite a bit more distance than other recent "bad days."

I am surprised to see the limited coverage of Amazon's recent shutdown of Google Shopping/PLA (picture ads) that show at the top of Google results related to products has been.

“Marketing firm Merkle noticed Amazon’s sudden retreat on April 28 by analyzing Google shopping ad data it tracks for clients. “The widespread vanishing act observed over the last week point to Amazon itself pausing its Shopping campaigns,” Andy Taylor, a Merkle research director, wrote in a recent blog.”

Most brands and retailers have become accustomed to Amazon typically outbidding them for position #1 in PLAs or at least being in the top 5. Alongside Amazon you will see other retailers battling it out along with the brand for placement. All of this competition leads to higher prices for better placement which ultimately helps Google.

I'd be surprised if Amazon wasn't the largest bidder on the PLA/Shopping platform and with Amazon dropping out, I'd expect bid prices to come down. Could they have dropped out because they know most customers (60%+) will start their search at Amazon anyways? Could they have dropped out because the cost of PLA (imaged ads) has become too high yet continued to pay for AdWords (text ads)? Sign of the war intensifying? Likely a mix but this is definitely a good thing for those with PLA budgets and not a good thing for Google.

“Competing against Amazon.com “is like racing against Secretariat or playing Michael Jordan,” he said. “A lot of things we were trying to do, they have done better.””

You don't typically see CEO's concede on their ability to compete with other industry players yet the outspoken Eddie Lampert of Sears has done just that. Lampert is not your conventional CEO. Lampert comes from a hedge fund & finance background and has carried out one of the largest real estate wind downs by selling off the low and medium tier Sears/K-Mart stores and spinning the higher tier into a REIT via Seritage Properties. No retailer has been able to compete thus far. Just think about the recent headlines. Walmart sold their Asda stake to pay for their battle with Amazon in India. Bonton is now bankrupt.

Some retailers realize the impact of Amazon and its reach within retail and outside of retail. Kohl's accepts Amazon returns that have led to positive traffic gains to those specific stores and a completely new customer profile. Chicos understands that 60%+ of the ecommerce growth is via Amazon and decides to list their product. Best Buy understands the importance of their private label and thus uses Alexa as their platform.

Regardless of Lampert's end goal with Sears/K-Mart, his brashness is spot on. No retailer can take Amazon head on and every retailer needs to carve their niche exploiting Amazon.

L2 recently interviewed author Derek Thompon on the debate of whether the distribution network and scale of Netflix is more valuable than treasure trove of content (Pixar, Star Wars, Marvel) that Disney owns. Fascinating listen on who will win over time and whether new entrants like Spotify have a chance. But is there only room for one?

I find it funny how we all talk about cord cutting because of our desire to stop paying for too many channels or content we don’t need yet switch to buying “channels” like Netflix, Hulu, HBO Go, Showtime Anytime, ESPN+ with an abundance of content we don’t watch. Bundles of these apps and services have begin with Hulu and Spotify being offered together and Google TV is now the equivalent of a Verizon FiOS or Time Warner cable bundle..

Because we are just recreating the same ecosystem we are fleeing, there won’t just be one. There will be many. And companies like Disney realize this. Hence they are “confusing” customers by splitting Hulu and Disney core content into two “channels.” Why?

Because adults will pay for both. They will purchase Disney streaming for the family and Hulu streaming for when the kids go to bed. Don’t count Bob Eiger and Disney out just yet, there are many more channels to come as traditional media brings their content back online. Have a listen, fascinating.

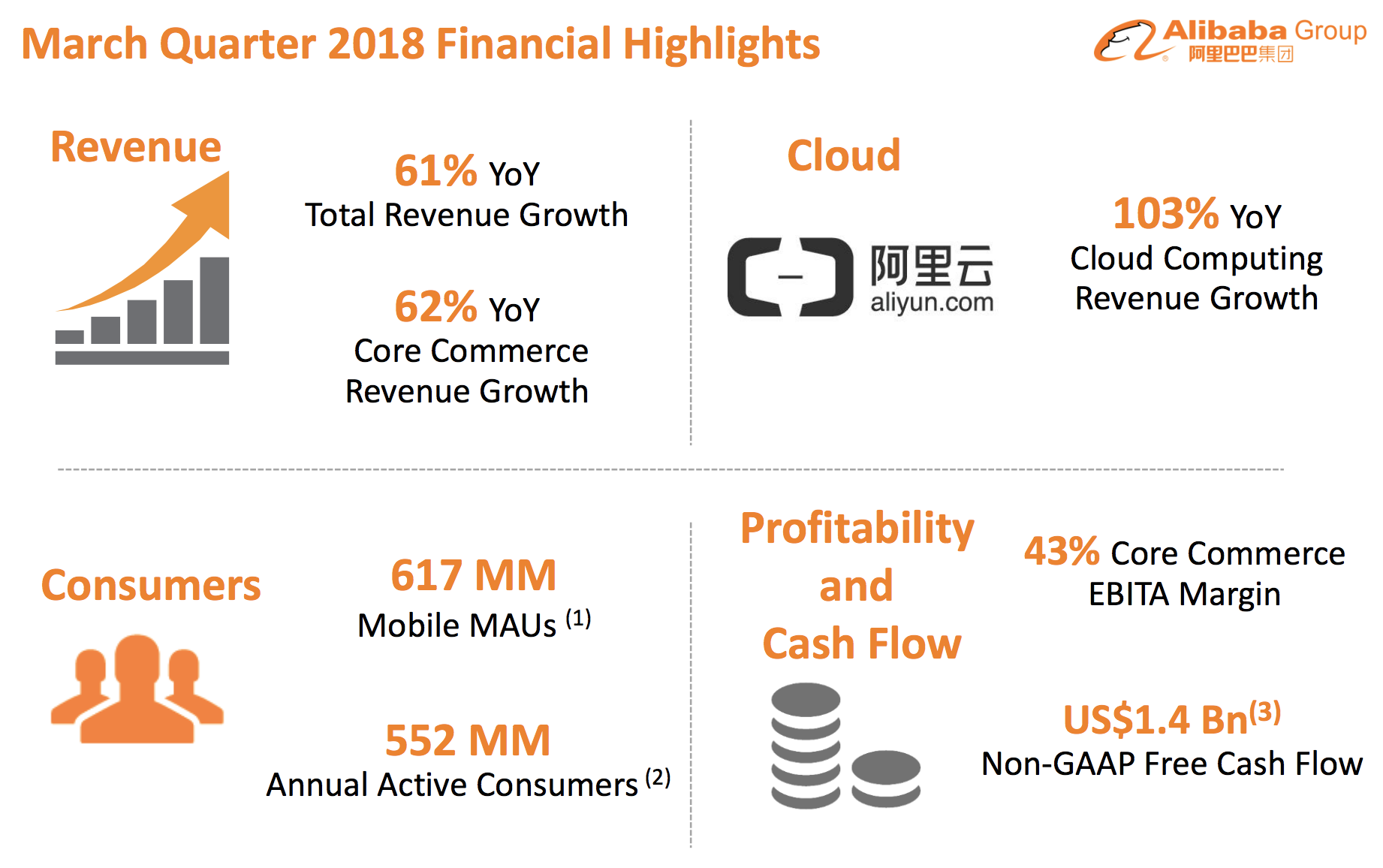

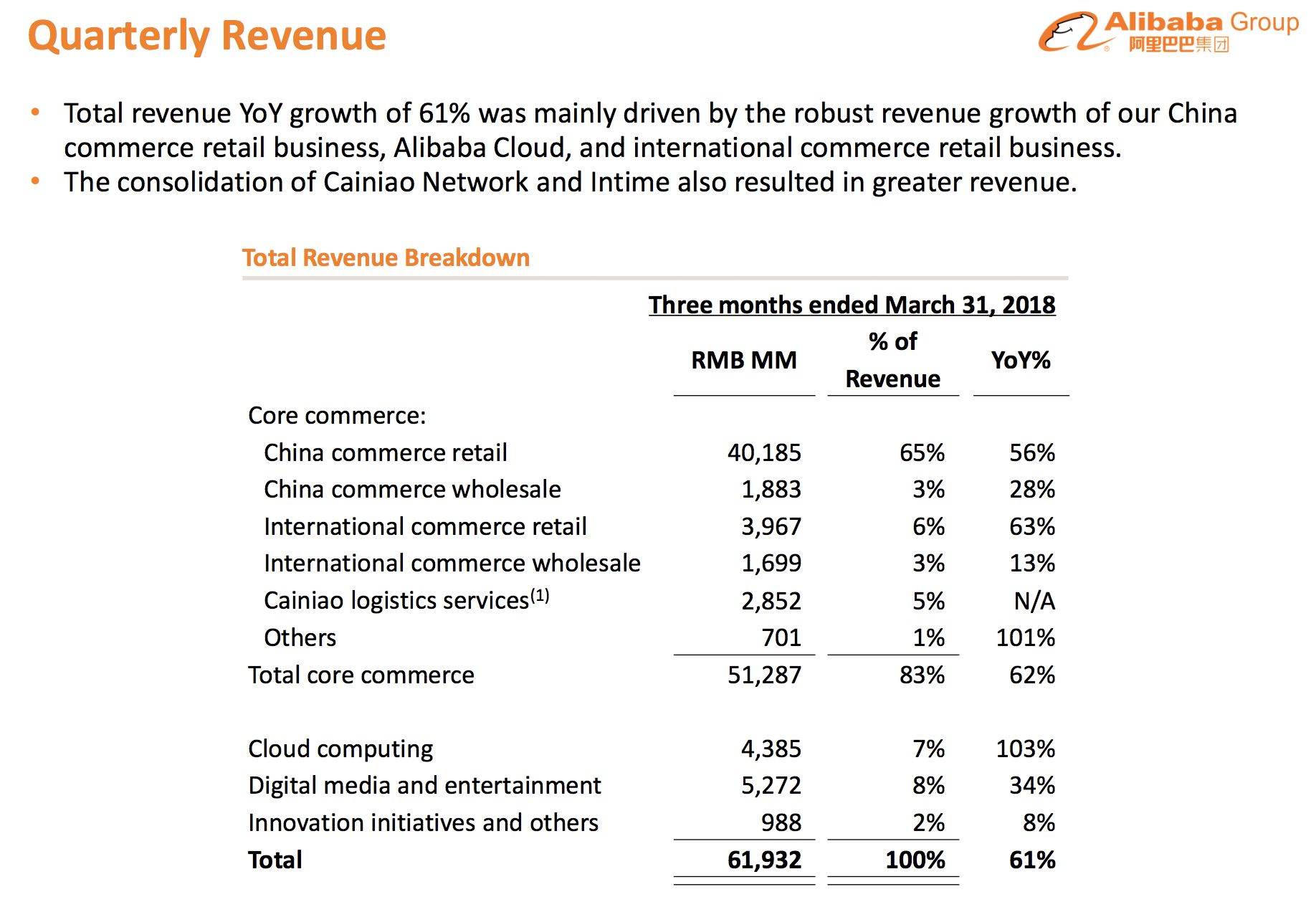

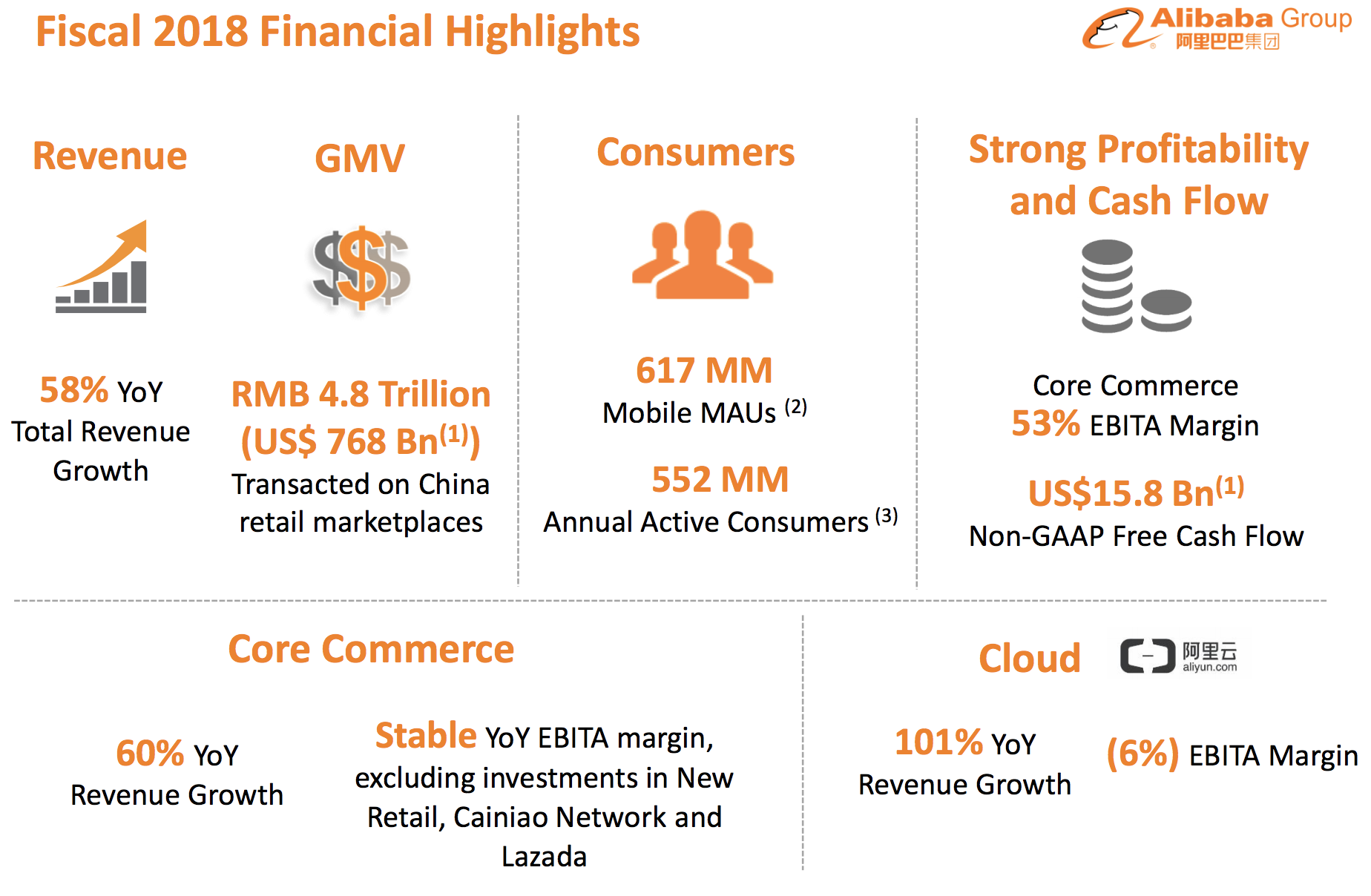

Although Alibaba is trading nowhere near the YTD return of Amazon, the latest quarterly results were astounding:

The strategy of Alibaba is very similar to that of Amazon, using the domestic cash flow and scale to fuel bets in content spend, international growth, cloud investments and the building of the largest domestic logistics network. I remain convinced that Alibaba has rosier days ahead and is certainly the best way to play the Chinese market's maturation into a consumer led economy.

““The value of Prime to customers has never been greater,” said Olsavsky. But, he says, it’s also expensive. “The cost is also high, as we pointed out especially with shipping options and digital benefits, we continue to see rises in costs.””

Don't be fooled. The increase in cost of Prime is a calculated move by Amazon on the stickiness of the program. Amazon continues to use the cash flow from their Prime membership base and AWS growth to invest in their international expansion and offset the cost of logistics. This is one lever they know will likely see very little churn with a 20% increase. Bezos' #1 job these days is about effective capital allocation and this a well played move.

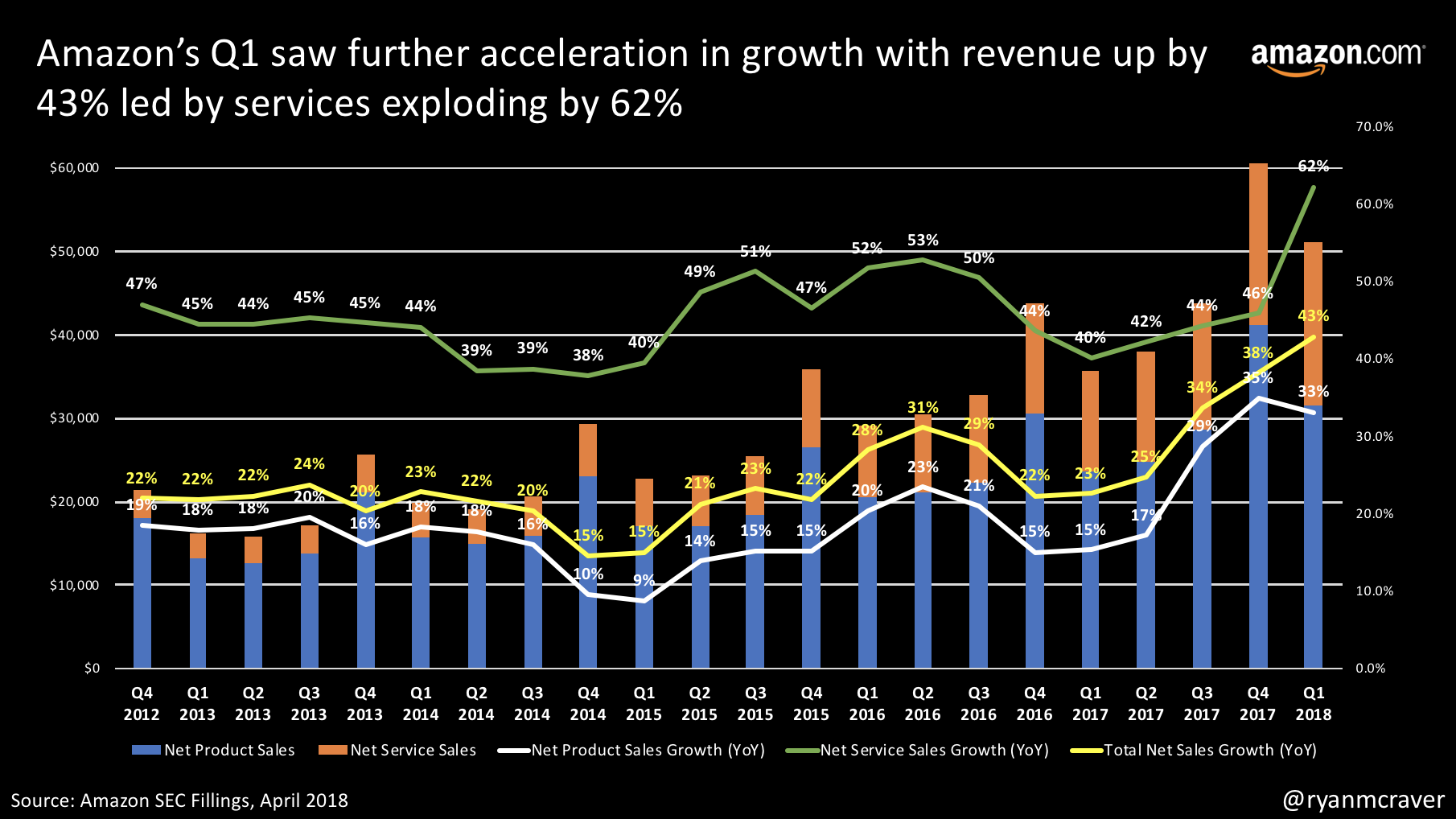

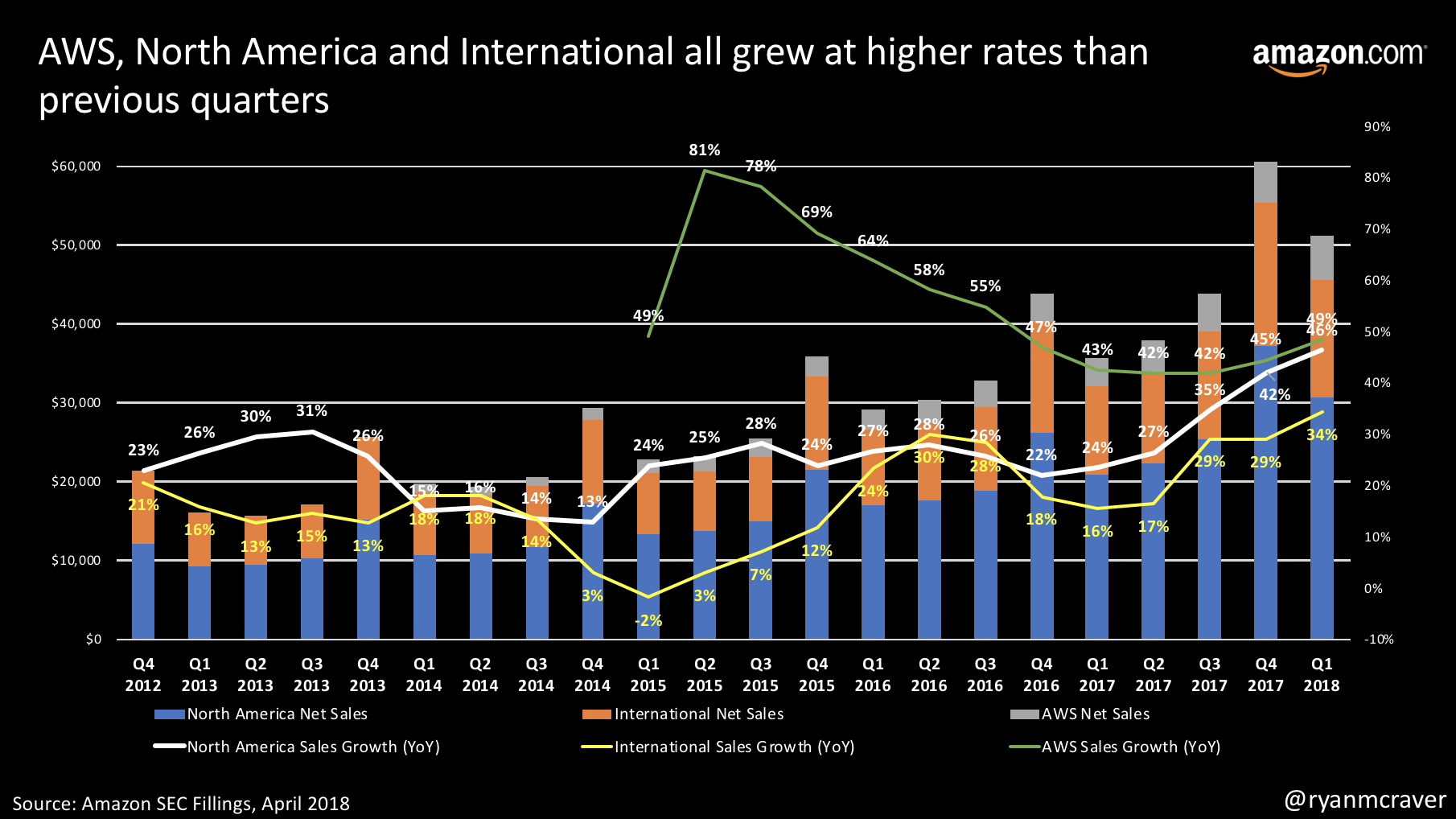

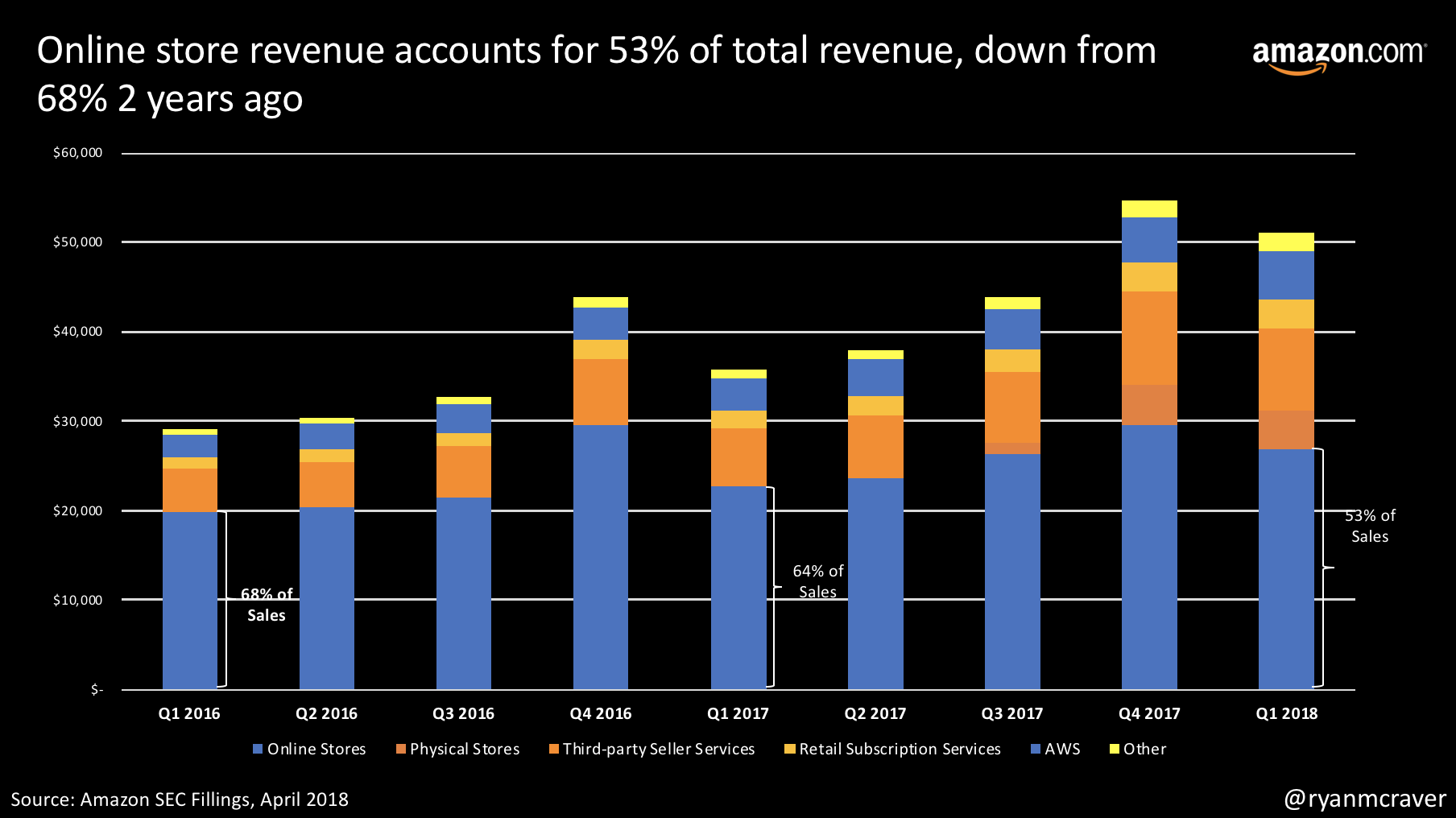

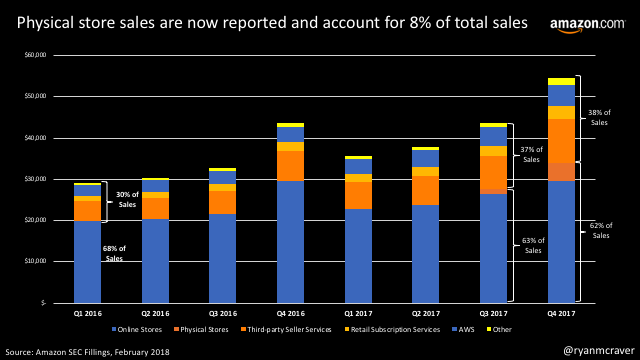

Amazon's latest earnings provided the services inflection we have been watching. Amazon's ad network, mix of cloud services, Prime memberships and marketplace/3rd party seller services now account for nearly 40% of revenue. Add on the Whole Foods brick and mortar sales of ~8% and you have an etailer that only drives 53% of their revenue from the online store.

Amazon continues to become the go to platform for selling, distributing and streaming everything from product to content. There is no slowing and profitability only improves as they become more of a service provider. Updated charts below.

A lot of chatter surrounding the Best Buy partnership with Amazon to begin selling Alexa powered televisions both on Amazon.com marketplace and within Best Buy stores.

So who wins? Both. Let's take the easier one first.

Amazon gains further reach into televisions for Alexa. Bezos wants Alexa everywhere. Amazon gains real world brick and mortar shelf space while also strengthening their online offering for televisions. A massive business for Amazon.

Best Buy gains a technology platform for their private label Insignia televisions, additional customers via Amazon.com and more products to fill their stores in the pursuit of being the store selling EVERY brand. Keep in mind, Best Buy already sells Amazon products in stores alongside Samsung, HP and Apple store-in-store concepts. Keep in mind, Best Buy already sells on eBay. Product placement on marketplaces like Amazon and eBay is a must in today's ecommerce world. I am shocked it took this long.

Most will call this a deal with the devil. I applaud both for seeking to exploit what each other needed.

“Schiefelbein: How vulnerable is CommerceHub to the increasing centralization of ecommerce by giants like Amazon?

Walker: Dropshipping penetration of ecommerce should grow as ecommerce players seek to compete with Amazon’s product assortment and cost and logistics advantages. Dropshipping can level the playing field with Amazon without the substantial infrastructure investments that company has made over many years. Long term customers of CommerceHub still only use dropshipping for 30-50% of their online sales. For many retailers dropshipping penetration is less than 10% of online sales. Given the benefits of dropshipping it seems logical that this penetration will increase over time.

For brands that wish to decrease reliance on retailers and sell products directly to consumers, CommerceHub for Brands can help them to achieve this goal. The internet and social media have expanded the number of ways in which brands can interact with customers. CommerceHub for Brands allows vendors to replicate their product lists and promotion across multiple demand channels directly, bypassing retailers.”

Every retailer I talk to these days is willing to start a dropship relationship (typically via CommerceHub) for literally any brand. It is easy to understand why. The retailer takes no inventory risk and allows for the buyer to quickly assess the brand's ability for success with a brick & mortar rollout. All the downsides are for the brand/manufacturer. The brand must ship a one piece order yet still only make wholesale on the shipment. This is why I believe dropship for retailers will never pan out to the industry's expectations. CommerceHub realizes this and is now focused on promoting their solutions for brands...extending a brand's reach to other platforms that aren't reliant on retailers...but reliant on marketplaces like Amazon, Facebook and Google.

Dropship isn't Amazon's achilles heel. Dropship will further empower Amazon.

Q4 is in the books. Earnings got off to a rough start with Walmart reporting ecommerce growth below the previous quarters 60% increases but picked up steam as department store mainstays surprised with positive comps. Commentary to be updated throughout the earnings season.

Department Stores

Off Price

I am often asked, "how should we sell to Amazon?" The answer varies for every brand but will typically take one of two paths.

For brands that have grown up in the wholesale world selling to specialty stores and brick and mortar retailers like Macy's, Target or Home Depot, the first inclination is to "sell to" Amazon. For brands who have grown up via direct to consumer channels, the first inclination is to "sell on" Amazon. Each model varies in margin, scale, level of effort and complexity and how the relationship works with the Amazon Buyer.

Brands preferring the "sell to" Amazon typically start with an Amazon Buyer meeting in which Amazon will purchase a handful of SKUs in various varieties to "set the store" with a standard template for co-op, freight and damages. All product setup, copy writing and keyword tagging is done by the brand while Amazon shoots the product. After the first delivery, the algorithms take over to reorder anything successful. The algorithms will suggest markdowns, promos and marketing with an anticipated sales lift. This dip the toe approach is beneficial to Amazon to weed out the selling potential of the brand's catalog and minimize risk.

While it may sound simple, there a couple of points to note:

The days of setting a brick and mortar store with loads of product, hoping for a 60-80% sell-thru and minimizing markdowns at season end is not the norm with North America's largest retailer. The personal connection with a retail buyer is no longer common. Algorithms are more efficient and effective with a bit of human intervention. Look no further than the announcement of job cuts that took place today.

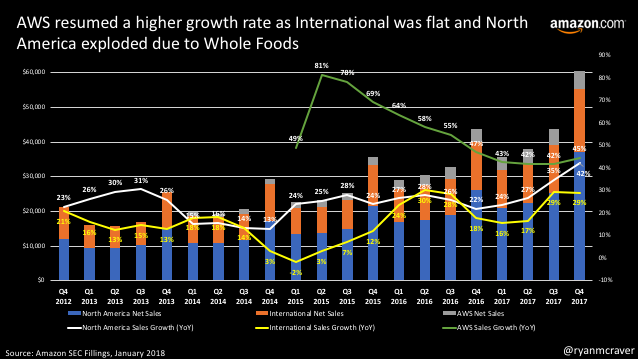

Another quarter with monstrous growth of which most was expected due to the Whole Foods acquisition. A few major themes:

Nothing to worry about here. However, as the effects of the Whole Foods growth disapears after 2 more quarters, international will need to ramp further to maintain the 30%+ growth rates investors are accustomed to. Updated charts below.

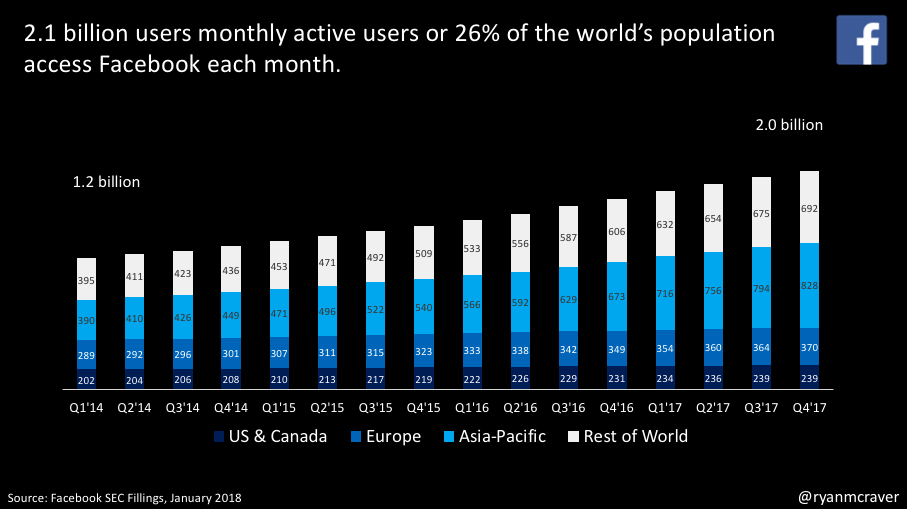

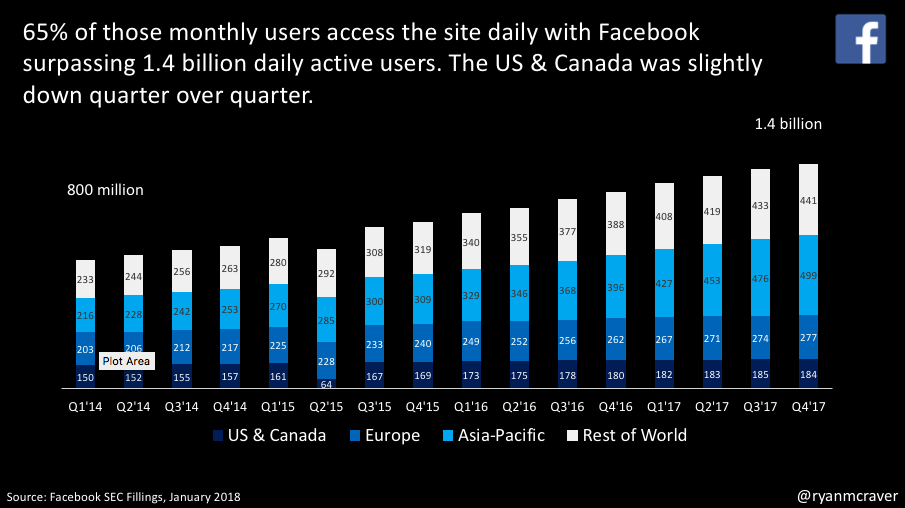

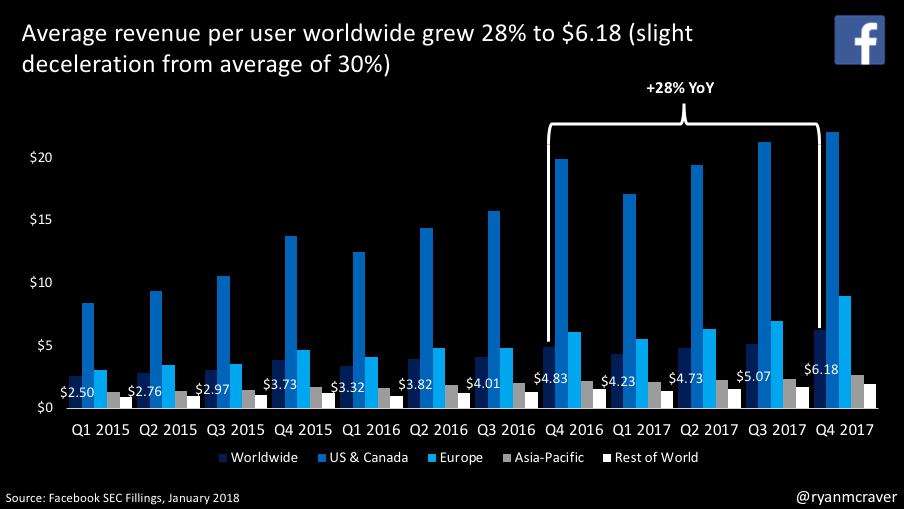

Despite the pessimism, Facebook continues to post strong numbers. Although the average user revenue worldwide growth came in at 28% which is below the average of last several quarters, the behemoth is now earning >$20 per user in the US and Canada. One point that I haven't seen in recent quarters is the daily users were down slightly in the US and Canada...otherwise the growth elsewhere is mind boggling. Nearly 1.5 billion people access the platform daily. Updated charts below.

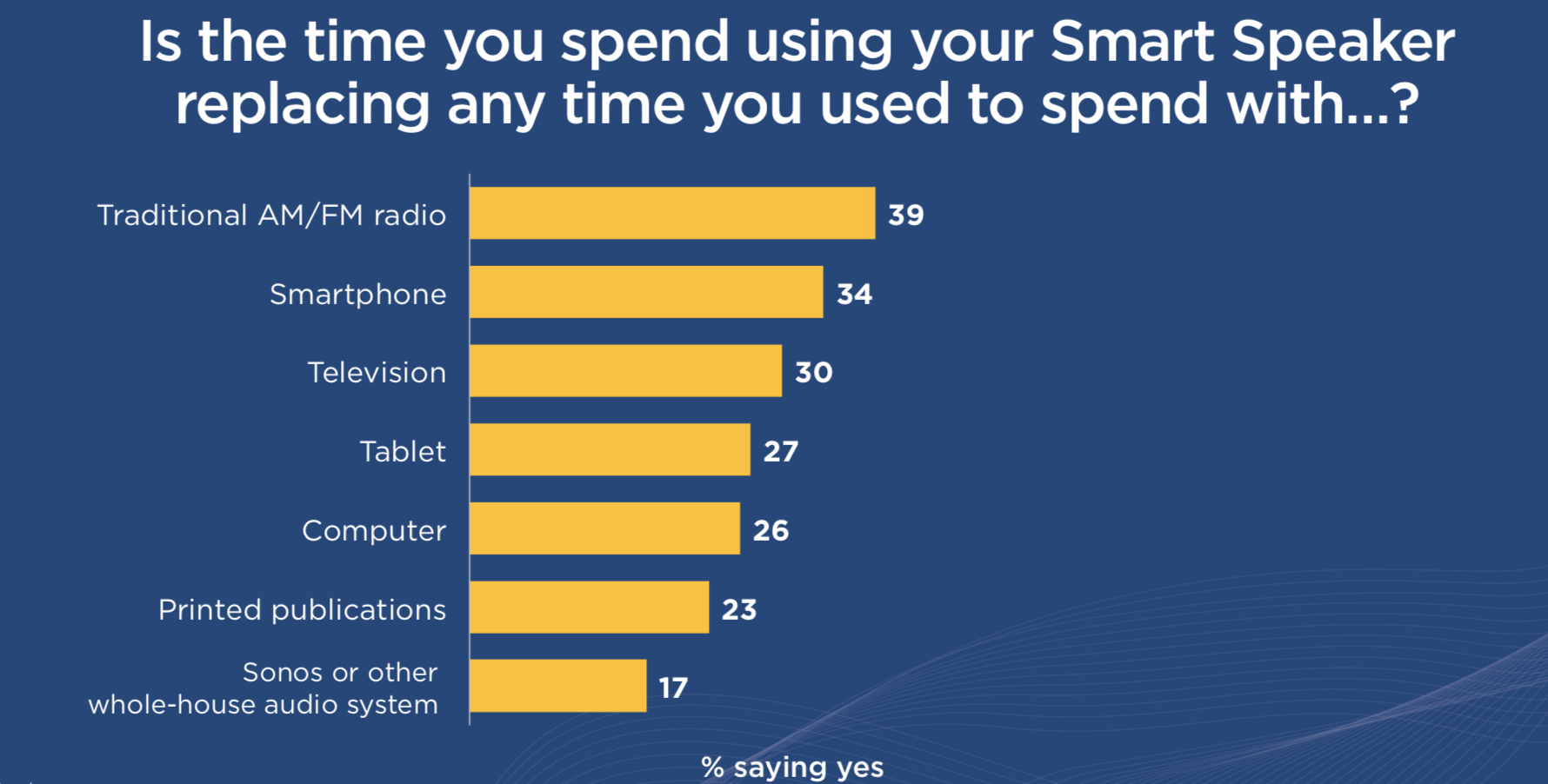

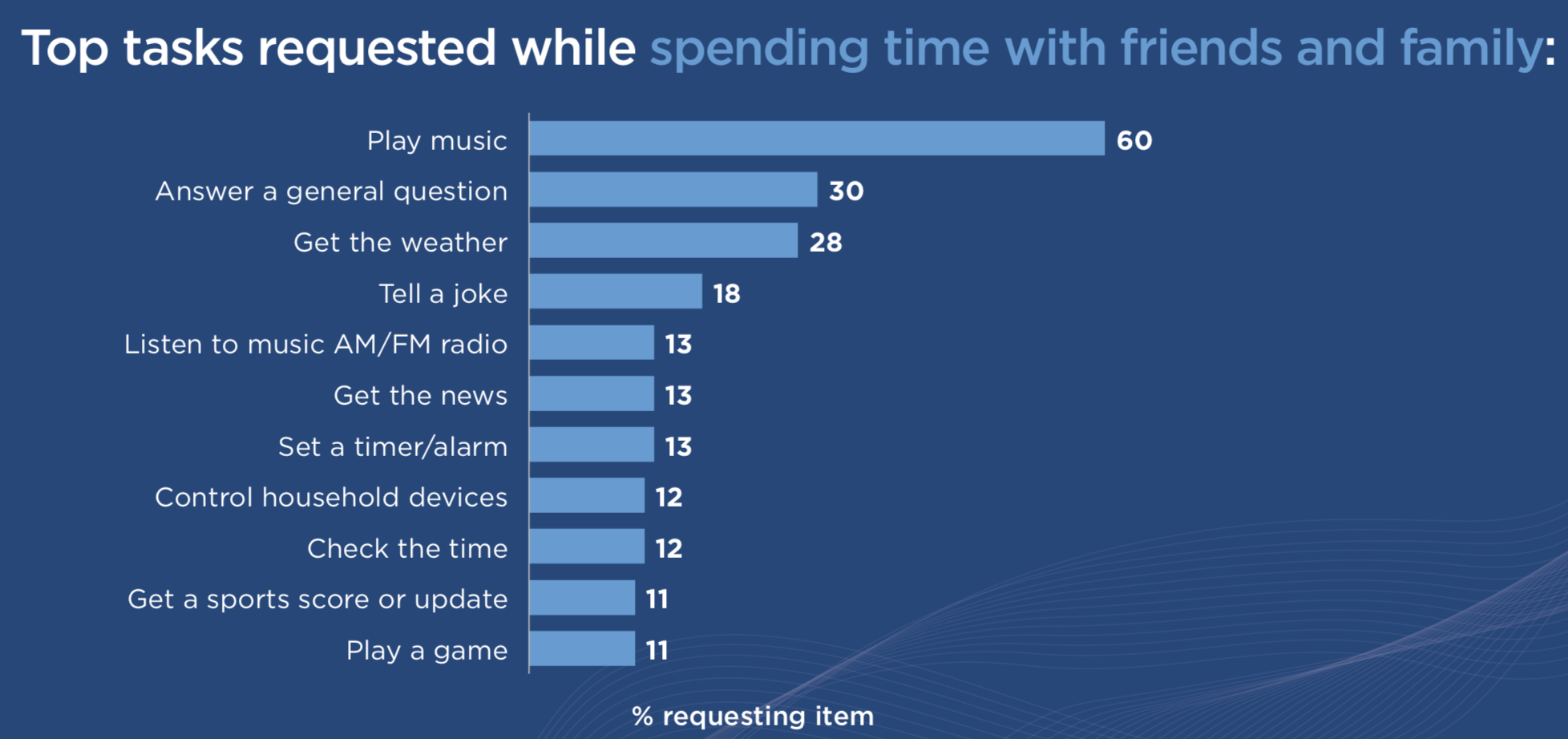

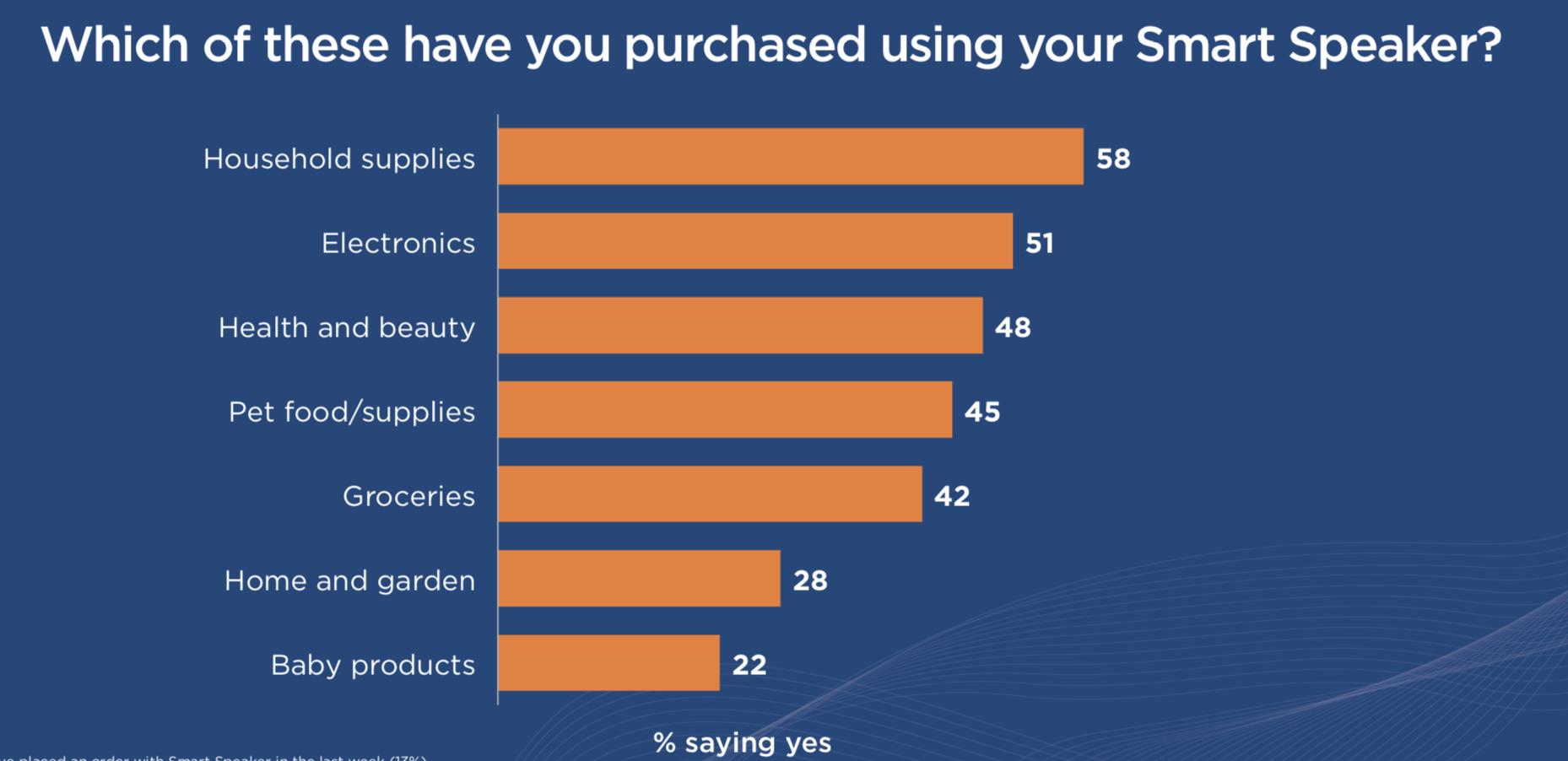

NPR and Edison recently released a state of the union report on the Smart Speaker space with responses from 1800+ respondents (note that 800 of the online respondents all owned a smart speaker). A couple of key takeaways:

Bottom line: Smart speakers have been firmly planted in the homes of millions with surprising results in browse and purchase habits.

Are we still addicted to email and are they worthwhile for retailers? A recent study by Fluent of 2,667 respondents believes so:

Bottom line: While we do receive too many emails, we are still addicted and emails continue to drive browsing and purchase behavior.

Although various outlets proclaimed Black Friday dead, there were a number of key takeaways:

Stay tuned for more news and takeaways as the 4 day shopping frenzy evolves.

Earnings season kicked off with the department stores bringing more of the same news on much lower expectations which resulted in some significant moves in stock prices. As the department store releases passed, we moved onto big box and off price. There are few remaining retailers with Hudson's Bay (Saks, Saks Off Fifth) and Burlington to report later this week.

Earnings season is off to a difficult start with department stores first to report. One recurring theme thus far is retailers either protected their margin and took the negative sales hit OR bought the quarter. Will update results as they funnel in.

Caught up on all things retail over the weekend: